UK property market update: Week 40, 2025

The UK property market in Week 40 of 2025 shows steady seasonal shifts. New listings dip slightly, sales remain strong, and rental prices continue their upward climb. Here’s a snapshot of the key trends shaping the housing landscape this autumn!

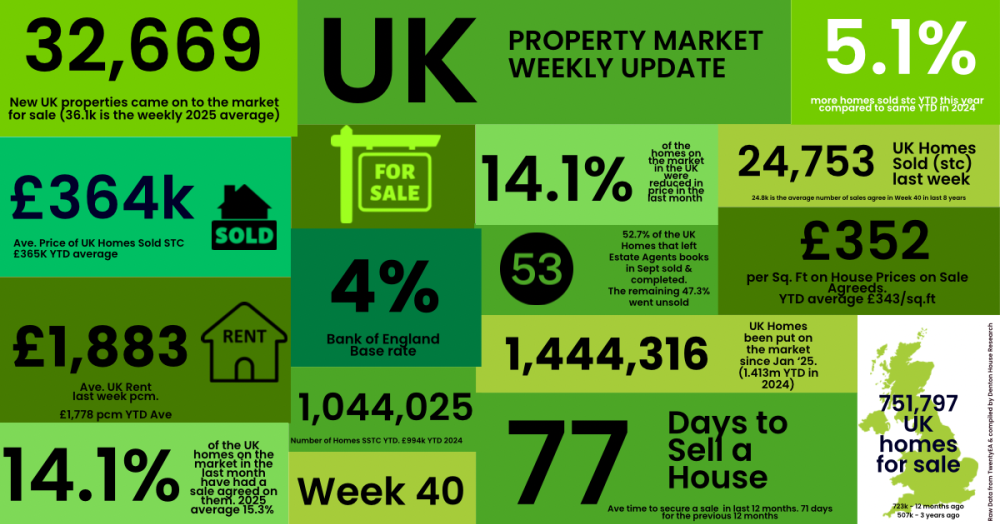

✅ New Listings

• 32.7k new properties came to market this week, down as expected from 34.3k last week.

•2025 weekly average: 36.1k.

• Nine-year week 40 average :33.4k

•Year-to-date (YTD): 1.44m new listings, 2.2% higher than 2024 YTD (1.41m) and 10% above the 2017–19 average (1.31m)

✅ Price Reductions

•24.6k reductions this week, slightly higher to last week at 25.6k.

•Increase in the number of homes on the market being reduced in September to 14.1%. In August, it was 11.1% (everyone must have been on holiday!), whilst it was 14.1% in July and 14% in June.

•2025 average so far: 13.2%, versus the five-year long-term average of 10.74%.

✅ Sales Agreed

•24.8k homes sold subject to contract this week, down as expected from 25.6k last week.

• Week 40 average (for last 9 years) :24.8k

•2025 weekly average : 26.1k.

•YTD: 1.044m gross sales, which is 5.1% ahead of 2024 (994k) and 13.2% above the 2017–19 average (922k).

✅ Price Diff between Listings & Sales

• Average Asking Price of listings last week £432k vs Average asking price of Sales Agreed (SSTC) - £364k

•18.7% difference (long term 9 year average is 16% to 17%)

✅ Sell-Through Rate

•14.1% of homes on agents’ books went SSTC in September.

•Down from 14.5% in Aug, 15.4% in July, 15.3% in June, and 16.1% in May.

• Pre-Covid average: 15.5%.

✅ Fall-Throughs

• 6,262 fall-throughs last week (pipeline of 510k home Sold STC).

•Weekly average for 2025: 6,562.

•Fall-through rate: 25.3%, up from 24.6% last week.

• Long-term average: 24.2% (post-Truss chaos saw levels exceed 40%).

✅ Net Sales

•18.5k net sales this week, up from 19.4k last week.

• Nine-year Week 40 average: 18.2k.

• Weekly average for 2025: 19.9k.

•YTD: 795k, which is 4.3% ahead of 2024 (762k) and 10% above 2017–19 (724k).

✅ Probability of Selling (% that Exchange vs withdrawal)

•Preliminary September Stats : 52.7% of homes that left agents’ books exchanged & completed. (Note this will change as more September stats come in in throughout October)

•August :55.8% / July: 50.9% / June: 51.3% / May: 51.7% / April: 53.2%.

✅ Stock Levels

•751k homes on the market at the start of October, 4% higher than October 2024. (723k)

•510k homes in sales pipeline on the 1st October, 2% higher than 12 months ago.

✅ House Prices (£/sq.ft)

•October 2025 agreed sales averaged £336.54 per sq.ft.

✅ Rentals

•Average Monthly Rents by region

· East Midlands - £1,070 (Growth since 2016) - 46.2%

· East Anglia - £1,396 (Growth since 2016) - 30.7%

· Inner London - £3,113 (Growth since 2016) - 24.9%

· North East - £968 (Growth since 2016) - 27.7%

· North West - £1,318 (Growth since 2016) - 64.1%

· Northern Ireland - £961 (Growth since 2016) - 41.1%

· Outer London - £1,948 (Growth since 2016) - 22.3%

· Scotland - £1,157 (Growth since 2016) - 52.2%

· South East - £1,619 (Growth since 2016) - 26.2%

· South West - £1,354 (Growth since 2016) - 48.3%

· Wales - £1,092 (Growth since 2016) - 44.4%

· West Mids - £1,092 (Growth since 2016) - 35.1%

· Yorks & Humberside - £1,031 (Growth since 2016) - 36.2%

•Average UK rent in September - £1,846 - a growth 2.44% from Sept 2024

•297k rental properties were available in Sept ’25 (286k - Sept 24 & 229k in Sept ’23)

If you would like to chat about our local property market, feel free to drop me a call on 01282 772048 or email me at info@pendlehillproperties.co.uk